No, I didn’t spell the title wrong – not Keynes. If you haven’t heard of Steve Keen, that’s not too much of a surprise because I hadn’t either, although I regularly visit sites in the economics blogosphere. Steve has an important message, but it’s unlikely you will hear much about it any time soon because it is just too radical for most orthodox economists, and many ordinary people who have drunk the mainstream economic Kool Aid, to wrap their minds around it.

Steve Keen is Professor of Economics & Finance at the University of Western Sydney. He has a new book out, Debunking Economics: The Naked Emperor Dethroned? that I have been plowing through for the past couple of weeks. It’s been an enlightening read with a perspective that settles in nicely with my analytical engineering mind. Keen takes on economics with a very skeptical mathematical eye, and in the process has managed to skewer most of the pillars of modern neoclassical economic theory. One example, the iconic crossing supply and demand curves, turns out to be just plain wrong for any modestly realistic economic system. The problems come when attempting to aggregate the supply-demand concept to include multiple commodities and variable preference. There is no simple single-valued solution for the aggregate supply and demand problem, which means that the price point is not uniquely determined.

Keen points out that many of the shortcomings of neoclassical theory are ignored or “assumed away” to allow for “general equilibrium” conditions to be realized. One of those assumptions that is patently ignored by most mainstream models is the existence of debt. What matters to standard macro models is the quantity of goods produced (supply) with market clearing price to satisfy demand. Money, when treated at all, is just another commodity much like apples or steel. Too much of it makes it less valuable, and vice versa. Credit and debit are considered to be safely ignored in aggregate “general equilibrium” models since they are just changes in the distributions and not fundamental to quantities of production.

The dominant neoclassical paradigm embodies a “general equilibrium” analysis. Perhaps it is the belief in Adam Smith’s almost magical “invisible hand of the market” that is supposed to bring us to equilibrium. Maybe it’s that the equilibrium assumption is required for neoclassical economic models to be tractable, or perhaps such simplifications are an excuse not to consider issues of inequitable distribution. Without external shocks, equilibrium models run long enough will produce flat-line graphs. As Keen points out, if you believe in such models it is difficult to see a depression coming.

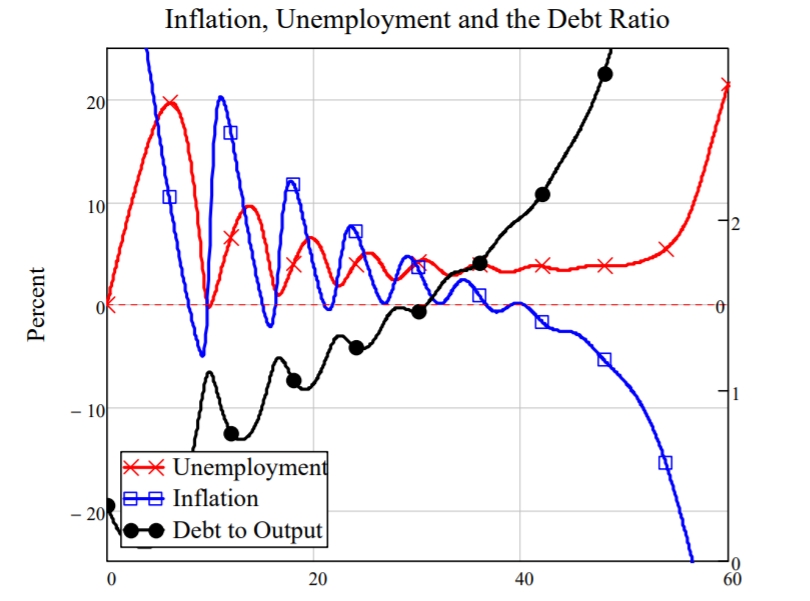

The best news is that Steve Keen has not only torn down the neoclassical edifice, but he has also managed to build some relatively simple but highly successful non-equilibrium economic models, built with a fundamental understanding of dynamic systems and some interesting economic insights as well. His models include money and debt explicitly. There are accounts for banks, workers, and firms with differential equations that specify how each entity interacts monetarily with the others. The model exists in time, so dynamic behavior is evident in the output. Keen includes a relationship that embodies the dynamics of the Philips curve that relates inflation and employment, and one that incorporates the dynamics of debt accumulation after Minsky. Below is an example run, where one can identify natural business cycles, a “great moderation” as the amplitude of the business cycles diminishes, and then a “great depression”.

Having a model that naturally generates behavior that we see in the economy is a starting point for understanding our dynamic world. Compare the model world with the same quantities for the real world below; not perfect by any means, but clearly some similarities in underlying dynamics.

[ Blogger lesson — keep the graphics with the blog piece — Several of the graphics for this post have been lost. Sorry GR 1/27/19]

[ Blogger lesson — keep the graphics with the blog piece — Several of the graphics for this post have been lost. Sorry GR 1/27/19]

One of Keen’s main points, and part of his models, is that spending power, or aggregate demand, is composed of ordinary income plus the change in the level of debt. This insight comes naturally from the Keenian understanding of the origin of money. In practice, monetary exchanges between parties is mediated by banks. Transfers between accounts are not limited to those with positive balances as long as the bank is willing to provide credit. Banks are motivated to make loans because interest on the loans are the primary source of bankers’ income. Keen argues that it is primarily the ability of banks to make what they consider to be profitable loans that determines the level of lending, rather than the reserve requirements mandated by government authorities. This point of view seems increasingly reasonable in an era where wealth is capturing more and more of the political process and co-opting any attempts at regulation.

Once the change in the level debt is included in the demand equation, it becomes much more apparent why the Great Recession has been such a big event.

The change in debt provides a positive feedback to the economy on both the upswing and the down. On the chart above, note that during the boom years 2000 – 2007, increase in debt was responsible for almost a quarter of our spending power. That situation rapidly ceased in 2008 as lending ground to a halt and went into reverse in 2009 – now reducing our spending power below our income as debt is repaid. The rapid change in the change of the level of debt (did you get that, this is the acceleration in the level of debt – the change in the level of aggregate demand) will affect the price we are willing to pay for goods. There is no better illustration of this effect than the correlation of this “credit accelerator” with the change in the price of housing.

The similarity is remarkable, with the biggest deviation coming during the irrational housing bubble years 2000 to 2007. When credit availability went south, house prices came tumbling after.

Take some time with Steve Keen. There is plenty to read on his website. Let his message sink in.

I don’t ordinarily comment on blogs commenting on my analysis,buti have to say this is a very well expressed précis of my analysis, and I appreciate it z great deal.

Please keep in touch Gary. I would also be pleased to have your engineering input on the program Minsky, as it develops. We are about to release the first alpha version, probably in March 2012.

Cheers, Steve Keen

Thanks, Steve. I did my best to condense your book into <1000 words!

I would be thrilled to get in on the ground floor of Minsky.

When I get some time I wanted to extend your QED monetary Minsky Model and add a government sector that would have some "automatic stabilizers" (unemployment insurance – progressive taxes) that would tend to transfer wealth back to the workers. I'd be curious to see if I could slow down the cycle times and reduce their amplitude…

Of coarse it could be the that the debt bubble just gets transferred to the government sector – or that the stabilizing effects allows private debt to grow even larger before serious consequences.

I thought this might be a nice first exercise to get my feet wet!

You did pretty well!

My 1995 paper “Finance and Economic Breakdown” adds a government sector to a stylized monetary model and finds the results you anticipate:

Click to access Keen1995FinanceEconomicBreakdown_JPKE_OCRed.pdf

But since it doesn’t model money creation and doesn’t have prices, those two additional dynamics aren’t explored.

It took me a good 15 years to go from the private sector model there to a full monetary model, and I haven’t yet incorporated the government sector in the monetary framework. However I think the path to doing so is prepared now, though QED itself does not make the modelling of the physical economy easy.

Minsky makes that easier, and it should be possible to generate two separate moey creation entities within the one table (though obviously the aim is to do it with separate Godley tables ultimately). I’ll be having a crack at it myself soon, though using Mathcad rather than Minsky in the first instance because I want to derive the equations for the system.

Ultimately doing likewise with Minsky is also a design objective–outputting equations in TeX–but that will take some serious coding.